Company Pensions

If you're looking at this section you're probably responsible in your company for employee benefits for staff. You may be in charge of an existing scheme or you may be looking to set one up. The following are likely to be some of your experiences or dilemmas:

Existing Pension Scheme

- The scheme was set up and other than a cost it means really very little to anyone

- Nobody is clear about the detail, least of all those who are supposed to benefit from it

- Getting an answer from anyone takes weeks, if not months, at the end of which you're not sure what you asked

- Staff get "benefit statements" that are unintelligible or at best ambiguous

- Any contributions are just a cost and asking for information just sets the fee clock ticking

- Investment returns are presented without any comparative context

New Pension Scheme

- You get a barrage of "helpful" invitations to sample wares from banks, brokers & insurance companies

- It's not always easy to spot the hidden agendas

- Should you go for a

PRSA Personal Retirement Savings Accountscheme or a traditional Company Scheme?

- The decision process is left to you with little guidance as to what's really important

- Nobody talks in simple language and not many understand that you're new to this

- It's hard, if not impossible, to get a clear service commitment or communication process

- There's seldom an offer to talk to the staff (who will ultimately benefit from all this)

- Jargon is the order of the day

Meritas are different - Why?

We've been around a long time and we've been dealing with pensions and pension schemes here in Ireland long before they were in vogue. We've dealt with the massive & complex pension schemes to the small and often equally complex arrangements for executives and small companies. Because of our experience we don't need to persist with the mystique around pensions, on the contrary we strive to demystify everything and speak without jargon for everybody's sake. This is our approach:

- If your company is spending money on a pension scheme it's a valuable benefit and needs to be appreciated

- As a consequence we will spend time with you explaining it so that there are no grey areas

- We will talk to the staff and members telling them what it is and how good it is

- We will even tell them individually how their financial planning is going in an overall sense

- When the insurance company sends you the standard computer generated bumph we'll explain it & fix it if necessary

- your insurance premiums are out of kilter, we'll make sure you get the best available

- If your fund performance is iffy we'll analyse it versus the alternatives and give you a critical assessment

- We believe in a niche approach and consequently you will always have access to advice at the top level

- There's nothing we haven't come across so you can feel secure in our knowledge and experience

Are we obliged to set up a pension scheme for our employees?

You are not obliged to contribute to a pension scheme on behalf of your employees but with effect from 15th September 2003 you will be obliged to provide access to at least one Standard PRSA (Personal Retirement Savings Account) to such employees as outlined below and to provide payroll deduction facilities for them.

Your employees must be allowed access to a

if:

- You do not currently have a pension scheme in place; or

- You have employees that are not included in the pension scheme; or

- You have imposed a waiting period for membership of 6 months or more; or

- You do not allow employees take out an

AVC Additional Voluntary Contributionsplan (within the scheme rules).

These rules apply to all employees, including temporary and part-time regardless of numbers of how small the workforce is.

We'd like to pay into a pension scheme for our employees but have no expertise. What are our options if we don't want to be trustees?

You have the option of appointing independent trustees to act on your behalf. Meritas has a trustee company which can act for you in this capacity. Setting up a company

scheme, however, has become the route of choice for most companies in recent times principally because there is no requirement for trustees and because the employees get the benefit of

options. Additionally you do not have any responsibility regarding the investment choice and performance of the

fund(s). Where there are key staff for whom the contribution limits under

are too restrictive then individual non

pension arrangements can be established for them separately.

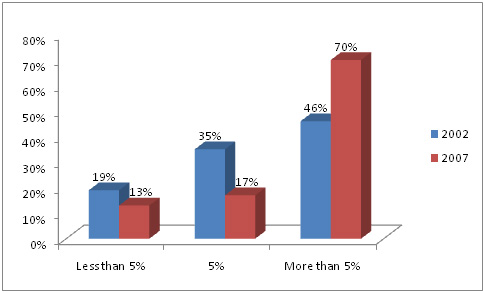

What do companies contribute on average on behalf of employees?

There is a wide variation across different sectors but there is evidence that the average contribution rate is 7% of salary plus the cost of insuring death and disability benefits on behalf of members. The Irish Association of Pension Funds carries out a survey every few years and the recent report in 2007 demonstrated an upward trend in terms of contributions since its previous survey in 2002. The following table is extracted from that report:

Why would we use a pension consultant like Meritas rather than going directly with an insurer?

Insurance companies provide the compliant structures so that contributions can be invested and ultimately the benefits can be paid out. Their specialisations are in the fields of investing and processing.

At its simplest, what you get from Meritas is an effective buffer between you and the institutional apparatus. Our role is to act on your behalf as a partner

- in achieving best value for money,

- in acting as experts for your HR in terms of employee benefits,

- in monitoring, analysing and reviewing investment performance

- in managing the day-to-day member queries

- in providing a comprehensive communications service to members including annual clinics

- in keeping the Company/HR/Trustees abreast with legislation changes

- in liaising with the insurers on all aspects of the scheme management

- in handling claims on your behalf from instigation to payment

- in ensuring everything runs smoothly with the minimum input needed from you.

Our experience and expertise in dealing with all aspects of employee benefits has been gained working with companies of all sizes over many decades. Equally we have developed our professional qualifications through education in pensions, taxation and investments as well as personal financial planning. Finally, in terms of cost, it will typically cost the same or less than dealing directly with an insurer because of the way their products are structured.

Self Administered

Self-directed plans, self administered schemes, private pension trusts became one of the "must have" accessories of the Celtic Tiger era reflecting the accruing wealth and sophistication of the burgeoning Irish entrepreneur.

Curiously the facility to set up a self administered pension plan has been around for decades and we have had "Pensioneer Trustee" status since the early eighties!

If you're reading this it's probably because you've either heard about them and want to understand more or you feel maybe you should have one. This link will give you a bit more information about them and their merits.

If you are really serious about one you probably need to understand what it involves:

- A Pensioneer Trustee approved by the Revenue effectively needs to set the whole thing up for you. Fundamentally the role is one of Revenue policeman!

- In essence all your company is doing is setting up your pension scheme without using an insurance company product

- The gains are transparency in everything and personal control over investment decisions

- The downsides are compliance requirements and costs, together with time commitments.

- Investment decisions are your own (when they go wrong as well as right)

- Where there is only one member the scheme is allowed to borrow subject to the ubiquitous terms & conditions

- As you might expect, there are some things you can't invest in like yachts, vintage cars, works of art etc.

- The Revenue requires that the Pensioneer Trustee is kept in the picture at all times and in particular is a joint signatory on all transactions

Feel free to call us to discuss whether or not a Self Administered arrangement would suit you.

Personal Pensions & AVCs

If you are self-employed or your employer doesn't pay into a pension scheme, putting money aside through a personal pension plan be it a

or traditional Retirement Annuity contract makes perfect sense. You can certainly save without using a pension structure but you will be missing out on the generous tax benefits.

Similarly if you are in a company pension scheme and want to add to your fund, Additional Voluntary Contributions (AVCs) are the way to go.

As people are now living longer and longer, a larger pension fund than ever before is required to ensure you can enjoy the comforts in retirement that you have become used to whilst working. With full tax relief available at your highest tax rate, and

relief,

are an extremely cost effective way to improve your financial status in retirement. You can make regular contributions, say monthly, or you can pay a lump sum on a once-off basis. It can also be possible to nominate a contribution to the previous tax year and get the tax back.

The portion of your fund attributable to

qualifies for the beneficial

options at retirement (see section on

below).

The two scenarios below illustrate why the savings structure you use is so important.

Example 1:

Bill has decided to save €150 a month from his take-home pay for the next 5 years in a deposit account yielding 4.5% per annum gross.

| Total Amount Saved | €9,000 |

|

Interest earned after

DIRT

Deposit Interest Retention Tax

|

€874.27 |

| Value of Savings after 5 years | €9,874.27 |

Example 2:

Had Bill taken a different approach and saved through his pension fund the outcome would be dramatically different. For the same reduction in his take-home pay of €150 a month he would have got the benefit of €254.24 a month because of tax relief (regrossed to account for 41% tax relief). The picture after 5 years and allowing for the same 4.5% yield would be as follows:

| Total Amount Saved | €15,254.24 |

|

Interest earned (

DIRT

Deposit Interest Retention Tax

won't apply)

|

€1880.86 |

| Value of Savings after 5 years | €17,135.10 |

These examples are simply to illustrate the tax benefit of a pension structure and they do not take account of the fact that the pension fund money will only be accessible at retirement and that tax may be incurred on the sum at retirement depending on choices made at the time.

The Cost of Delaying

A salutary tale.

Aisling and Breda, both aged 20, start work together on the same day and on the same pay. They share the same apartment and split their expenses equally. During the first month at work, they attend a presentation in work where they learn about the benefits of taking out a

Aisling decides to sign up and her contribution of €50 a month is matched by the same amount from the company. After tax relief it cost Aisling €37 a month. Breda, however, wants to wait until she is older before starting to save. Allowing for pay increases and a return on savings of 6% a year Aisling accumulates €24,800 after 10 years. Seeing this Breda now aged 30 decides to join the scheme. By the age of 60, Aisling's retirement account would be about €400,000, while Breda's account balance, started 10 years later, would be about €266,000.

Tax relief on contributions

You get tax relief on contributions to approved personal pension arrangements. This relief is more generous as you get older.

| Age | Percentage of Earnings |

|---|---|

| Under 30 years | 15% |

| 30 to 39 years | 20% |

| 40 to 49 years | 25% |

| 50 to 54 years | 30% |

| 55 to 59 years | 35% |

| 60 and over | 40% |

The maximum rate also applies to people in certain occupations and professions, irrespective of age where there is a limited earnings span. These occupations include professional athletes.

There is a ceiling of 254,000 euro on the earnings that may be taken into account. This limit will be increased in line with earnings from 2007.

You no longer have to buy an annuity with the proceeds of your pension policy, however, you may do so if you wish. This option does not apply in general to occupational pensions, but it may apply to the Additional Voluntary Contributions (AVCs) paid by people in occupational pension schemes.

Limit on overall value of fund

The Finance Act 2006 introduced a limit on the value of an individual's pension fund which may attract tax relief. The limit is the amount in the individual's pension fund on 7 December 2005 or 5 million euro whichever is the greater. This will be adjusted annually from 2007. If the fund is greater than the limit then tax at 42% will be charged on the excess when it is drawn down from the fund.

Transfer between funds

You do not have to remain in the same pension fund. You may transfer funds accumulated with one insurer to another fund with another insurer. Of course, there may be costs involved in doing this.

When you retire, you may opt for the existing annuity arrangements or for the new arrangements. The new arrangements mean that the accumulated fund is your property. You must take your pension not later than your 75th birthday (the previous upper limit was 70).

Approved Minimum Retirement Fund

You may take up to 25% of the fund as a lump sum (tax-free). Then you must set aside at least 63,486.90 euro of the fund and place it in an Approved Minimum Retirement Fund (AMRF). This fund may not be drawn down to less than 63,486.90 euro until you reach 75. This obligation to invest in an

will not be imposed if you have a guaranteed pension or income for life from a state pension, annuity or occupational pension of at least 12,697.38 euro per annum (this is called the minimum income requirement).

Approved Retirement Fund

After investing in the

you can then simply take the balance of the funds or you may invest them in an

or a number of such funds. If you take the funds, you will, of course, have to pay tax on them. An

can be any fund, including a bank account, in a regulated financial institution. Income tax is payable if you draw down these funds.

From 2007-2009 a tax on those parts of the fund which are not drawn down will be phased in. The tax will be 1% in 2007, 2% in 2008 and 3% from 2009 onwards and will apply to

created on or after 6 April 2000.

After death

If you die before taking any benefit from your fund, the accumulated funds form part of your estate and are distributed accordingly. Capital Acquisitions Tax may apply.

If you die after taking benefit and you have invested in an

the remaining funds form part of your estate but are regarded as your income in the year of death. Tax at your marginal rate is deducted and the remaining amount is distributed in the normal way. There is no

liability. However, if your spouse inherits the funds, no income tax is payable. Effectively, your spouse steps into your shoes as owner of the fund and when he/she dies, a 20% rate of income tax may be payable and there is no

liability. This is the case unless the funds are inherited by children over 21 - in this case, the amount they get is taxable as the child's income in that year, but taxed at a flat rate of 20% rather than at the child's marginal tax rate.